Dear all,

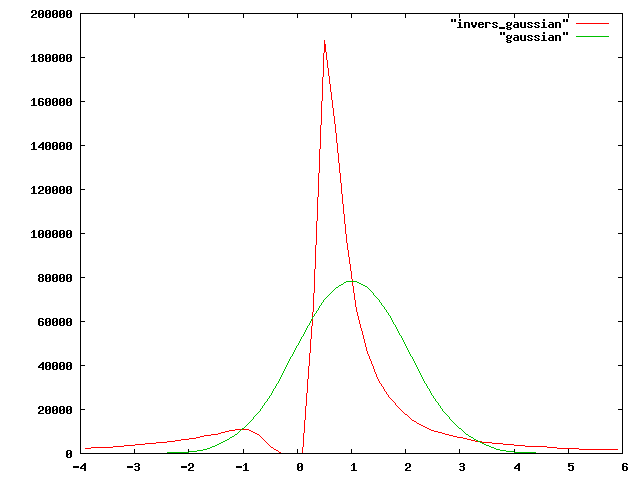

just to show what I mean where the problem is: I've produced 1 million

Gaussian random numbers with a mean of 1 and a standard deviation of 1.

I attach a plot showing both the Gaussian itself, and the distribution

of the numbers obtained by taking the inverse. The latter looks quite

non-Gaussian to me.

According to the formulas in Wikipedia and John Taylor's book the

"inverse distribution" should also have a mean of 1 and a sigma of 1.

But this is not the case. Its standard deviation is 437 (a different

random number would give a different number here!), due to its long

tails that arise from those values of the original distribution that are

close to 0. The Wikipedia's "error propagation" article in its "Caveats

and Warnings" paragraph calls this a Cauchy distribution.

This is clearly an example where the first-order approximation breaks

down, and common sense tells me that this happens because we may divide

by numbers close to zero.

And it shows that it might be useful to think about error propagation,

and not blindly apply the formulas.

thanks,

Kay

-------- Original Message --------

Subject: Re: Question about the statistical analysis-might be a bit off

topic

Date: Tue, 7 Jun 2011 11:28:50 +0100

From: Ian Tickle <[log in to unmask]>

Kay, the usual propagation-of-uncertainty formulae are based on a

first-order approximation of the Taylor series expansion, i.e. assuming

that 2nd and higher order terms in the series are can be neglected.

This is clearly not the case if B is small relative to its uncertainty:

you would need to include higher order terms. See the 'Caveats and

Warnings' section in the Wikipedia article that Bernhard quoted.

Cheers

-- Ian

On Tue, Jun 7, 2011 at 8:59 AM, Kay Diederichs

<[log in to unmask] <mailto:[log in to unmask]>>

wrote:

what I'm missing in those formulas, and in the Wikipedia, is a

discussion of the prerequisites - it seems to me that, roughly

speaking, if the standard deviation of B is as large or larger than

the absolute value of the mean of B, then we might divide by 0 when

calculating A/B . This should influence the standard deviation of

the calculated A/B, I think, and seems not to be captured by the

formulas cited so far.

best,

Kay

Am 20:59, schrieb James Stroud:

The short answer can be found in item 2 in this link:

http://science.widener.edu/svb/stats/error.html

The long answer is "I highly recommend Error Analysis by John

Taylor:"

http://science.widener.edu/svb/stats/error.html

If you can find the first edition (which can fit in your pocket)

then

consider yourself lucky. Later editions suffer book bloat.

James

On Jun 4, 2011, at 10:44 AM, capricy gao wrote:

If means and standard deviations of A and B are known, how

to estimate

the variance of A/B?

Thanks.

--

Kay Diederichs http://strucbio.biologie.uni-konstanz.de

email: [log in to unmask]

<mailto:[log in to unmask]> �Tel +49 7531 88 4049 Fax 3183

Fachbereich Biologie, Universit�t Konstanz, Box 647, D-78457 Konstanz

This e-mail is digitally signed. If your e-mail client does not have the

necessary capabilities, just ignore the attached signature "smime.p7s".

|

{kind=link}